Calculating a Transition Support Payment

Getting an idea of your payment

You can use the following information to get an indication of the maximum Transition Support Payment you may be entitled to receive.

However, your actual payment amount will be calculated by Callaghan Innovation once you have applied and provided all of the necessary information.

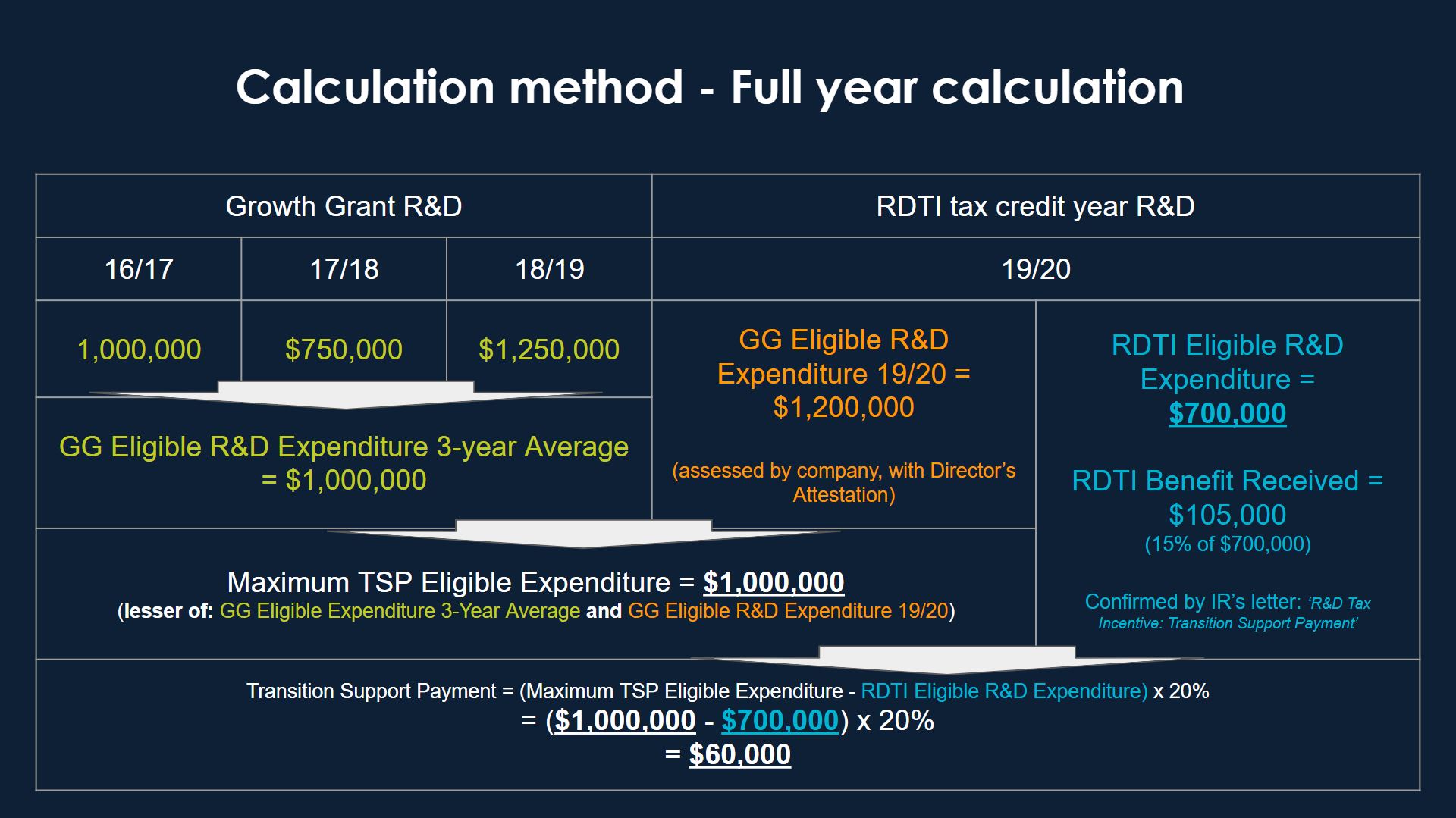

How a full-year payment is calculated

The following example shows how a full-year Transition Support Payment is calculated:

The calculation for a full-year Transition Support Payment is:

(Maximum Transition Support Payment Eligible R&D Expenditure

minus

RDTI Eligible R&D Expenditure)

X 20%.

Definition of terms used in calculation

|

Maximum Transition Support Payment Eligible R&D Expenditure |

This is whichever is the lower of the following:

|

|

Growth Grant Eligible R&D Expenditure 3-year average |

This is the average of the business’s Growth Grant Eligible R&D expenditure in the 3 years immediately preceding the year in which the Transition Support Application is made. Callaghan Innovation calculates this figure after reviewing Growth Grant payments made to the business, aligned to the business’s income year (i.e. not aligned to the Growth Grant contract year or the financial year end reporting timeframe, if these differ from the income year) |

|

Growth Grant Eligible R&D Expenditure |

This is expenditure that would have been eligible for the Growth Grant (had it continued) in the year in which the Transition Support Payment application is made. A business must accurately self-assess this figure and provide it to Callaghan Innovation with a Directors’ Attestation. |

|

RDTI Eligible R&D Expenditure |

This is the amount of R&D expenditure confirmed by Inland Revenue as eligible for the RDTI in the relevant year. If your R&D does not fit the RDTI eligibility criteria, this figure will be zero. A business must provide Callaghan Innovation with Inland Revenue's ‘RDTI: Transition Support Payment’ letter, which details the final decision oft an RDTI application. |

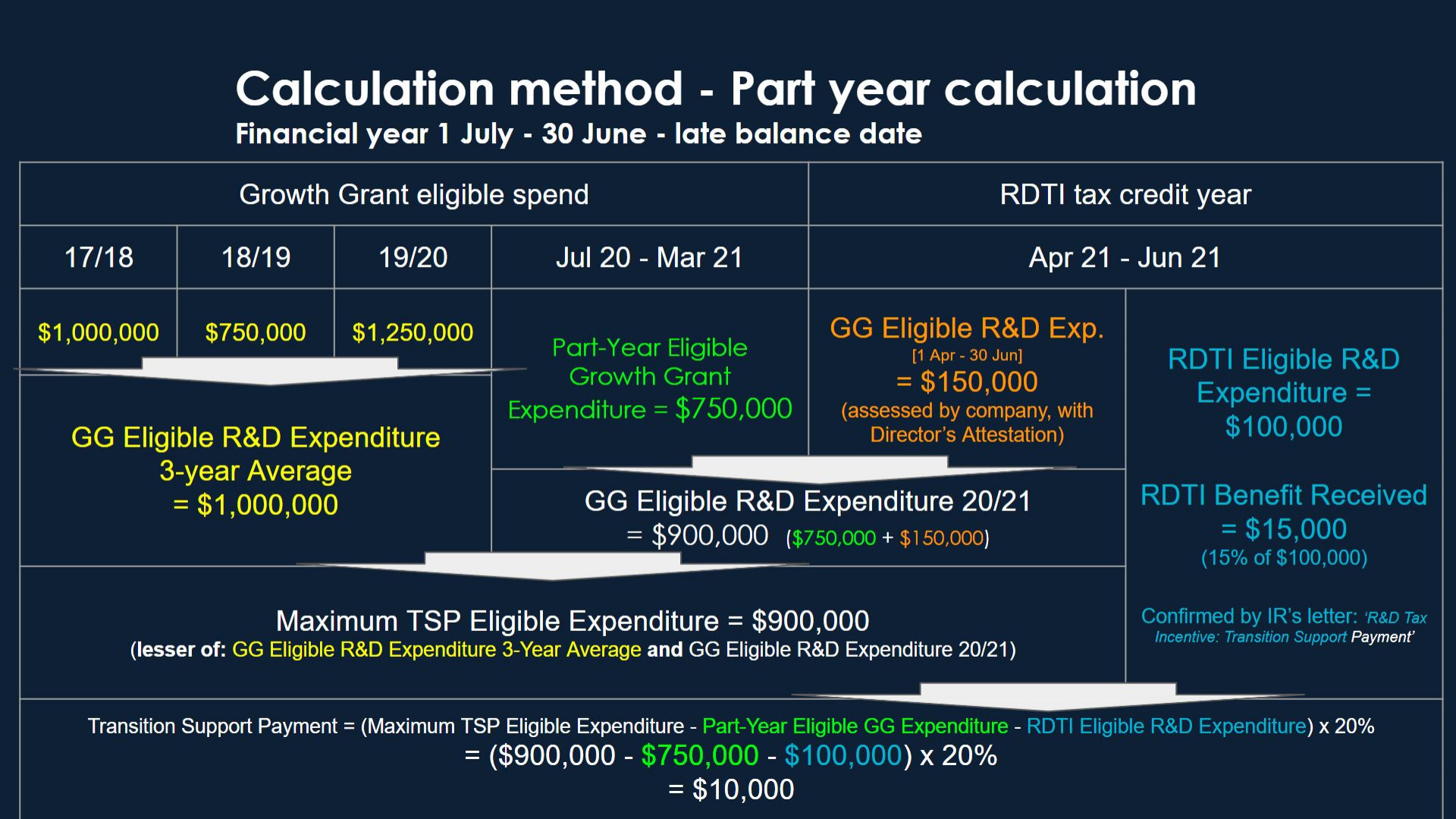

How a part-year payment is calculated

The following example shows how a part-year Transition Support Payment is calculated:

The calculation for a part-year Transition Support Payment is:

(Maximum Transition Support Payment Eligible R&D Expenditure

minus

Growth Grant Eligible R&D expenditure (Part Year)

minus

RDTI Eligible R&D Expenditure )

X 20%.

How the part-year calculation differs from the full-year calculation

The formula for calculating a part-year Transition Support Payment is similar to that used to calculate a full-year payment. However, because Growth Grant payments were received for part of the year, the ‘Growth Grant Eligible R&D Expenditure’ for the year includes both of the following added together:

- Growth Grant Eligible R&D Expenditure, assessed by Callaghan Innovation, for the period for which the business received Growth Grant payment, AND

- Growth Grant Eligible R&D Expenditure, self-assessed by the business, as if the Growth Grant had continued for the period in which the business participated in the RDTI.

The resulting amount is compared with the ‘Growth Grant Eligible R&D Expenditure 3-Year Average’, and the lowest of the two used as the ‘Maximum Transition Support Payment’ Eligible R&D Expenditure.

When calculating the part-year Transition Support Payment, the Growth Grant Eligible R&D Expenditure for the part-year for which the business received Growth Grant payment is deducted from the Maximum Transition Support Payment Eligible R&D Expenditure, along with the RDTI Eligible Expenditure.